Why Quantee?

Next-generation dynamic insurance pricing software

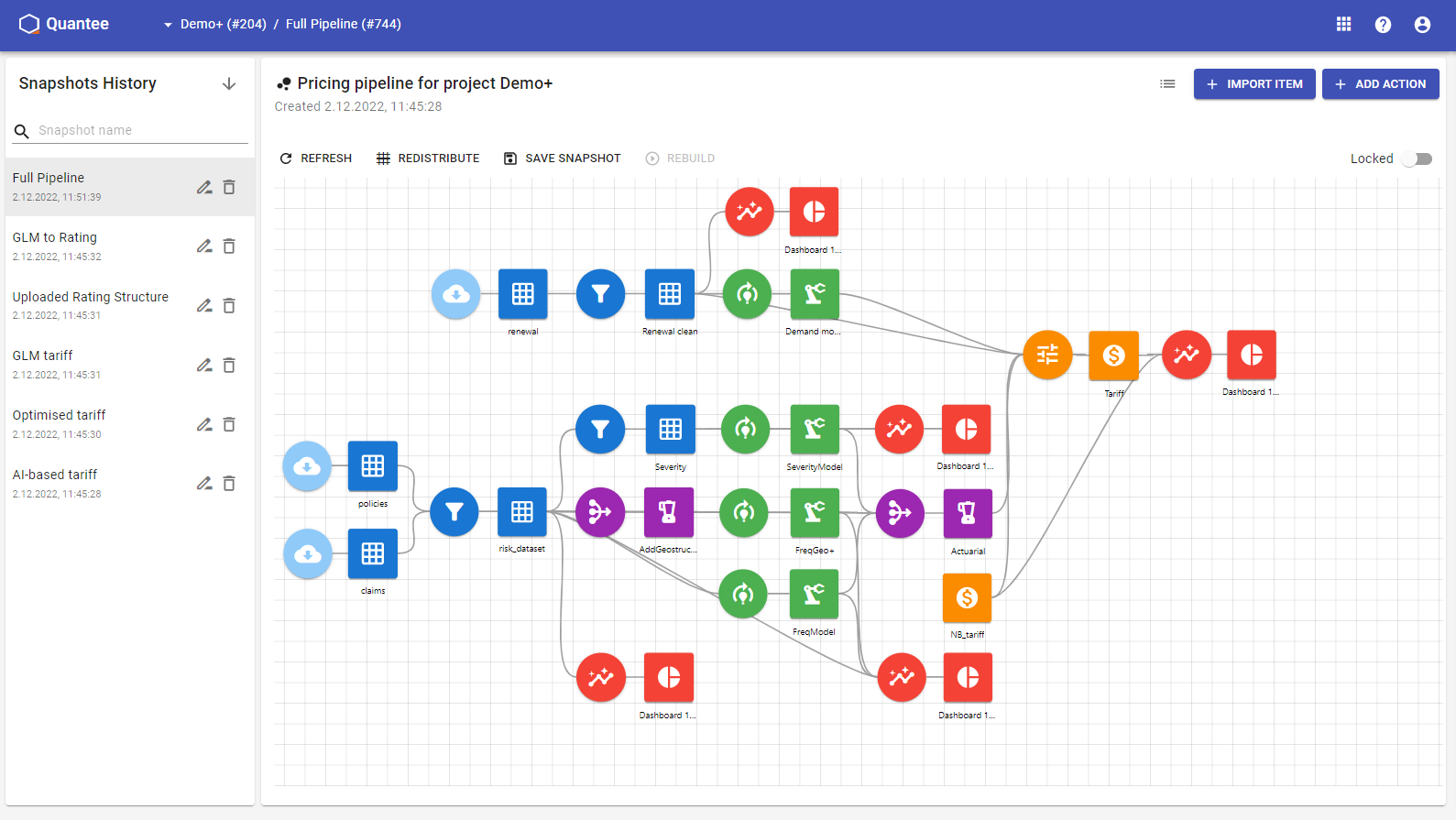

End-to-end solution

Get rid of fragmented and ineffective pricing architecture and see how much efficiency you can achieve with an integrated platform.

Peace of mind

Focus on your business and building the best tariffs on the market. We’ll take care of maintenance, performance and scalability.

Automation

Forget about boring, repetitive and manual tasks. You can use Quantee to automate them and have more time to do things that matter.

Endless possibilities

Would you like to extend the capabilities of the Quantee? Feel free to write your own plugins in Python and use them within the solution.

Easy collaboration

Use built-in features to share, copy or embed one project in the other, making collaboration between team members quick and easy.

Explainable AI

Get your superpowers using AI to build more powerful models while keeping a full transparency of the results