Does Moving Forward Always Mean Getting More Sophisticated? Thoughts on Insurance Pricing Challenges in LATAM

When we talk about innovation in the world of insurance pricing, it’s easy to fall into the trap of thinking that moving forward always means bringing in the latest machine learning tools, optimization techniques, or advanced elasticity and demand models. But after working closely with insurers across the region, we’ve learned that the reality is much more nuanced.

In many LATAM markets, it’s not (yet) about being on the cutting edge of technology, but about building a strong and practical base to build on. And that often means going back to the “basics”:

- Strong interdepartamental coordination,

- A pricing engine that understands your models,

- Solid data quality and governance,

- Models that are explainable and auditable,

- The ability to give answer to regulators,

- The agility to adjust rates and strategies in real time

Here are some of the real challenges we face – beyond the buzzwords.

1. Data Quality and Governance: Without Transparency, No Technique Will Work

One of the biggest challenges we’ve seen is the lack of transparency, traceability, and governance in the data flow between intermediaries and insurers. In many companies, data arrives late, incomplete, or in inconsistent formats. Historical records are often scattered across multiple silos with no clear structure or standardization – turning any attempt to modernize pricing into a technical nightmare.

On top of that, there’s the reality of many internal processes: legacy systems, manual operations, and no clear rules for handling data. This often leads to:

- Time and resources wasted on cleaning data,

- Information being lost along the way,

- Variables being renamed without traceability,

- Each department working with its own “version” of reality.

This not only undermines technical pricing but slows down any effort in analysis, segmentation, or optimization. In the end, the pricing team spends more time putting out fires than adding value to the business.

Because without a clean, reliable, centralized, and well-governed database, any predictive model is nothing more than a mathematical illusion.

How does Quantee help in this context?

Even if the original data quality is still a challenge, Quantee ensures full traceability throughout the entire pricing process – improving governance, transparency, and auditability.

With our platform, you can:

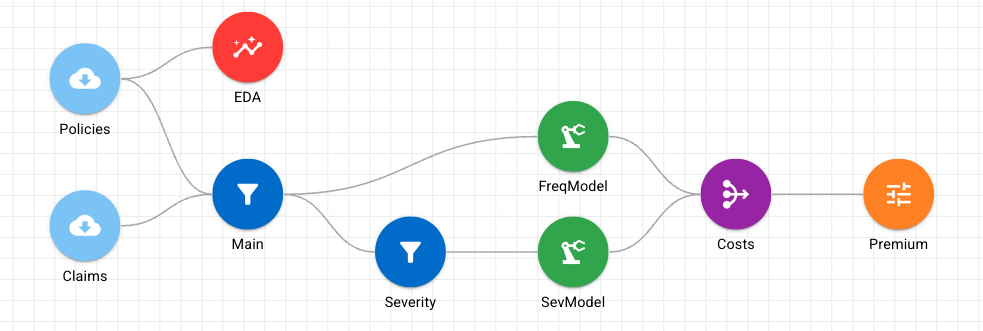

- Import data from a file or connect directly to your data lake, seamlessly integrating it into the pricing environment,

- Clean, transform, and enrich data with just a few clicks – no coding required.

- Create derived or synthetic variables to better capture risk behavior and support more robust explanatory models.

- Automatically document every step, making it easier for technical, business and compliance teams to work together.

And the most importantly, we’re there for our clients every step of the way. Our actuarial Product Success team offers expert support and market insight. With hands-on experience across multiple regions – LATAM, Europe, the UK, South Africa, Canada and Asia – we bring an international perspective and proven best practices that help interpret data, optimize processes, and accelerate analytical maturity.

With Quantee, data stops being a headache and becomes a strategic lever.

2. In-House, Legacy-or Simply Nonexistent-Models

Another reality we’ve come across is that, in some cases, insurers aren’t even working with their own models. Some still rely on:

- Factor tables inherited years ago that live in an old Excel file,

- Standard off-the-sheld rating tools,

- Or even models designed by the parent company in another country, despite4 local conditions being completely different.

Why does this happen? There are several reasons:

- Lack of adequate tools,

- Lack of technical profiles or enough volume to justify an in-house pricing team.

- And, quite often, a company culture that still hasn’t embraced the value of local, technical pricing.

3. Good Intentions, Bad Practices (forced)

In cases where more advanced models do exist, we often see a common pattern: Teams know they are not following best practices but they are limited by the tools they have or by regulatory requirements.

Common examples include:

- Versions with no traceability,

- Variables that are hard to explain or can’t be audited,

- Struggles to justify to the regulator why a certain rate is applied to a segment.

This isn’t due to a lack of willingness or knowledge – it’s due to the absence of a solution that brings together technical modeling, clear model explanations, and automatic regulatory reporting.

How does Quantee help in this context?

The answer isn’t (yet) to build deep neural networks or Bayesian optimization models. In many cases, the real improvement comes from having a tool that connects pricing, technology, auditing, and business.

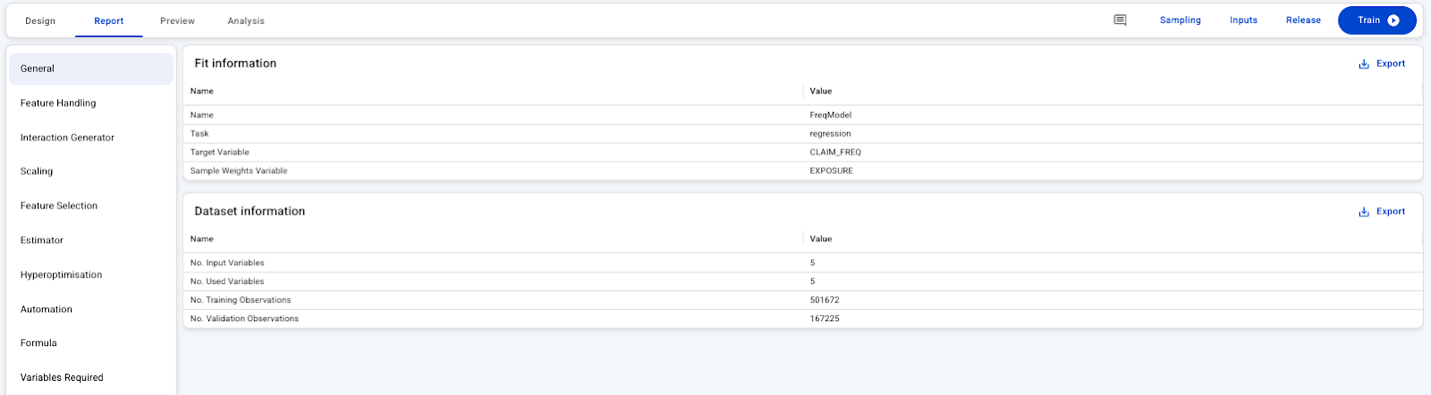

Imagine being able to:

- Build your technical model (GLM, GAM, etc.),

- Generate automatic reports with all variables, factors, formulas, and justifications.

- Adjust your rates quickly, with full traceability and audit support.

- Do it all through an interface that works for actuaries, business users, and regulators alike.

It’s not about doing what’s most complex – it’s about doing what’s most useful, optimal, and efficient

4. The Pricing Engine: When Changing a Rate Becomes an Odyssey

One of the most common bottlenecks for insurers is the pricing engine. Even with a solid technical model, getting that model into production and applying it dynamically can still be an operational nightmare.

Some of the most frequent challenges include:

- Lack of smooth connection between the analytics environment and the pricing engine.

- Rate changes that require IT tickets - leading to days (or even weeks) of waiting.

- Full dependence on IT for small tweaks or testing.

- Limited ability to run A/B testing, which slows down experimentation and learning.

- Scability issues, especially in lines like auto or fleet.

The result: a slow, inflexible process that falls short of what’s needed in a competitive, price-sensitive market.

How does Quantee help in this context?

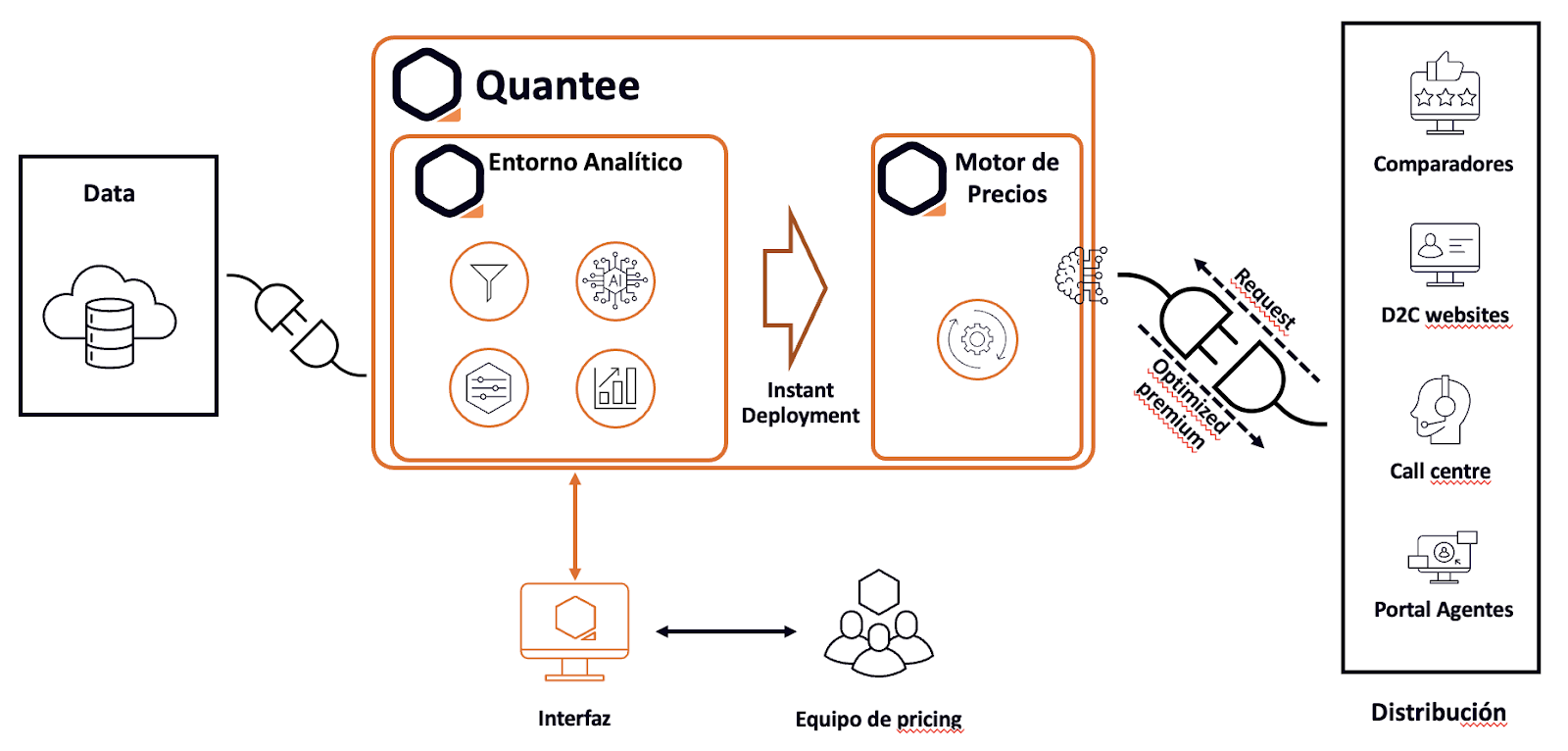

Our solution: a fast, connected, and frictionless Pricing Engine

From our experience, the key is to seamlessly connect the analytics environment with the pricing engine – efficiently, and with full control in the hands of the business or pricing team.

Our platform offers:

- Direct API connection between models and the pricing engine (request-response time in milliseconds)

- Lightning-fast record response times without losing traceability

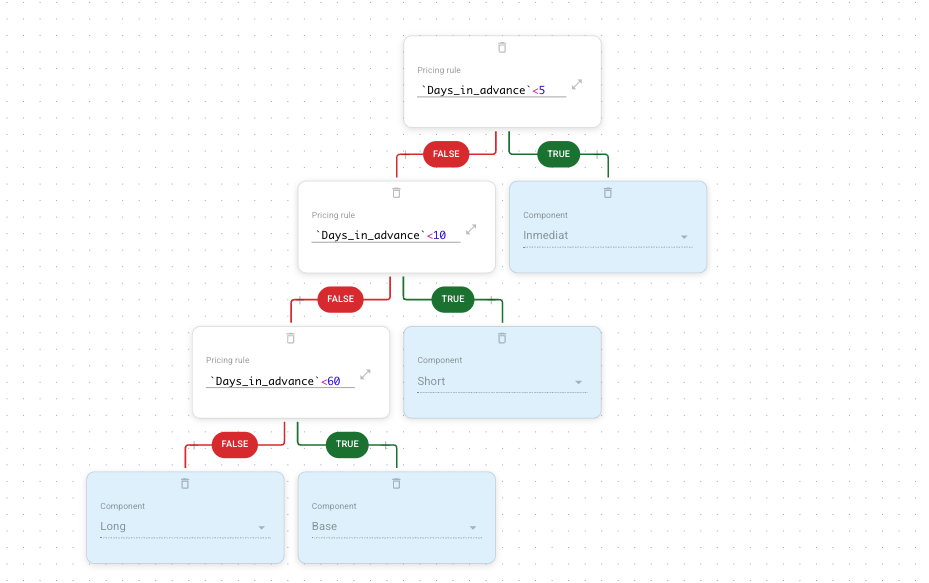

- Configurable business rules, built as decision trees, to apply different rates by segment, distribution channel, or promotions.

- One-click rate deployments - no dependency on it

- User and role management to control who can make the changes

- Batch capabilities for mass pricing, ideal for fleet or broker quotes

This type of tool doesn’t just solve operational problems – it frees the pricing team to focus on what really matters: analyzing, optimizing, and delivering strategic value

Conclusion: Moving Forward Also Means Simplifying

In LATAM, the real leap toward modernizing pricing isn’t (yet) about ultra-sophisticated models—it’s about getting the basics right: reliable data, explainable models, flexible tools, and response times that keep up with the business.

Often, the challenge isn’t in the theory—it’s in the operations, the internal culture, and the lack of tools aligned with the local reality.

At Quantee, we believe that innovation is also about simplifying, standardizing, and empowering technical teams with tools that help them work smarter, not harder. Progress doesn’t always come from what’s most complex—it comes from what truly transforms the day-to-day work of the pricing team.

It’s not about running before you can walk. It’s about building a strong, future-ready foundation and winning small battles that pave the way for real technical evolution.

That’s where we aim to be a strategic partner—not just a software provider.