Portfolio management in insurance pricing

P&C and health pricing teams live in an ever-changing environment – they need to make sure that the current pricing strategy is not only “right” for their policyholders, but also correctly embedded in evolving competitive and regulatory landscape. Pricing executives are in fact insurance portfolio managers, making sure that margins, loss ratios and GWP are constantly monitored and aligned with an insurer's overall strategy and market competitors’ landscape. Moreover, most recent regulations such as Customer Duty1 in the UK, proves that the ability to spot in real-time risk outliers within the portfolio and explain the source of these outliers in front of regulators is not only a nice-to-have but also a requirement.

Surprisingly, many insurance companies lack the proper technology, data integration and implementation knowledge behind portfolio management and monitoring.

In this post we will focus on key areas of portfolio management:

- Real-time data feed

- Monitoring dashboards

- Portfolio alerts

- Integrated reaction & forecasting

making an introduction to the best practices around this crucial topic.

Real-time data feed

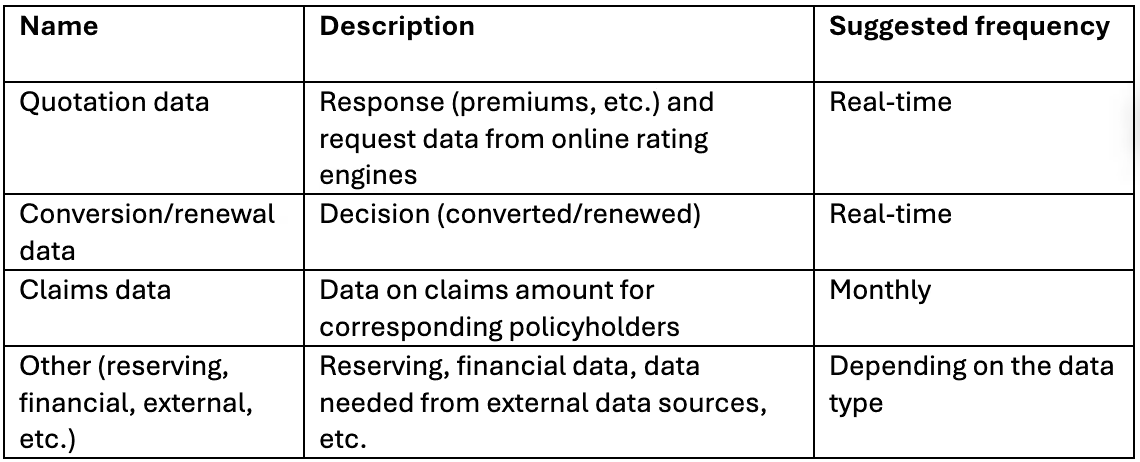

One of the challenges that insurance companies face early on their way to perform effective portfolio management is collecting all of the data needed. These are the types of data commonly used to monitor performance of the portfolio:

The main challenges around feeding these data sources are:

- Connecting portfolio management tools with quotation data coming from rating engines, including the complexity of different business lines, sales channels and multiple versions of production pricing strategies.

- A time offset between quotation and decision of potential policyholder to convert/renew and issues with collecting this data.

- Connecting to other data, such as claims, financial and external. Particularly maintaining a constant link between quotation data and claims/other data sources may be challenging.

A single but powerful advice:

Insurers should invest their time & resources now to clean up the data sources and unblock any potential benefits coming from real-time portfolio management. The earlier this is done, the lower the probability of losing a competitive position in the market.

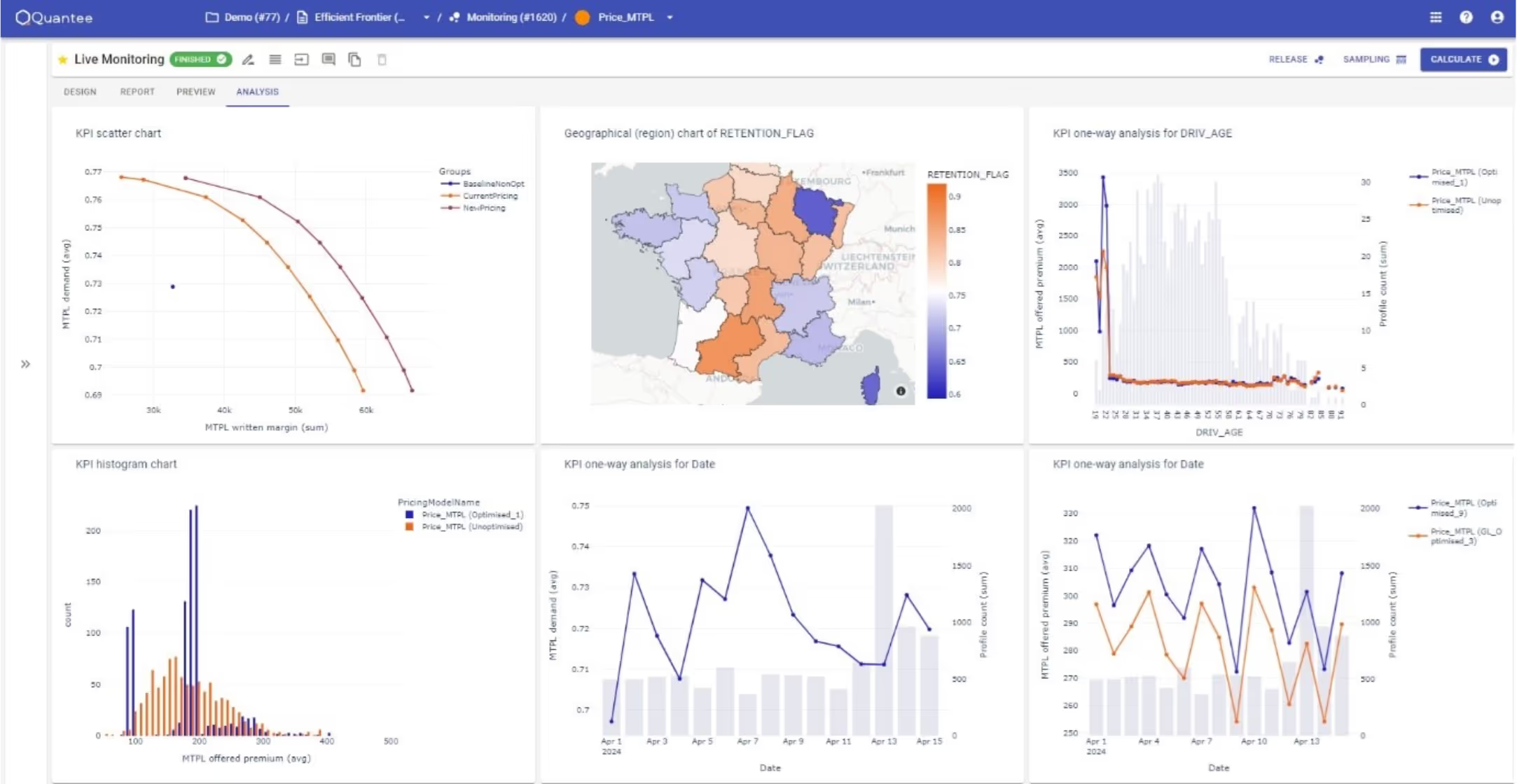

Monitoring dashboards

An ability to recognize underperforming segments, control the portfolio structure and make informed pricing decisions starts with proper monitoring capabilities. These should satisfy the following criteria:

- Being able to consume real-time data feeds and further adjust/process them for insurance executives' and pricing team's purposes.

- Contain pricing-specific charts, such as impact analysis, one-ways, loss ratio histograms/heatmaps and so on. These are usually not available in generic BI tools; thus one has to invest either in open-source or actuarial software.

- Being flexible enough to perform drill-down analysis for specific segments and interaction of segments as well as show overall portfolio performance.

Needless to say, monitoring dashboards are a bare minimum for any executive to make informed decisions on pricing strategy. What makes a competitive advantage are the next two topics: automated portfolio alerts and embedded forecasting/reaction capabilities.

Portfolio alerts

Insurers can reduce their combined ratios by up to 6 p.p. which translates to billions of dollars if only they can deal with time-consuming fragmented pricing process2. Time-to-market has become a crucial factor for pricing teams to improve and measure, mainly due to the competitive market, everchanging regulatory landscape and expectations of digitalised policyholders.

One of the areas to improve in the pricing process is the reaction time between a certain event in the insurance portfolio (for instance conversion drop for a specific segment) and the moment the pricing team realize the event happened.

A major idea to reduce the time-to-market is to utilize the real-time quotation/conversion data in algorithms that recognize the patterns in the portfolio and inform pricing executives about underperforming segments or dangerous outliers. This has even more priority for countries such as the UK in which Customer Duty regulation forces insurers to actively recognize and explain risk outliers in their portfolio.

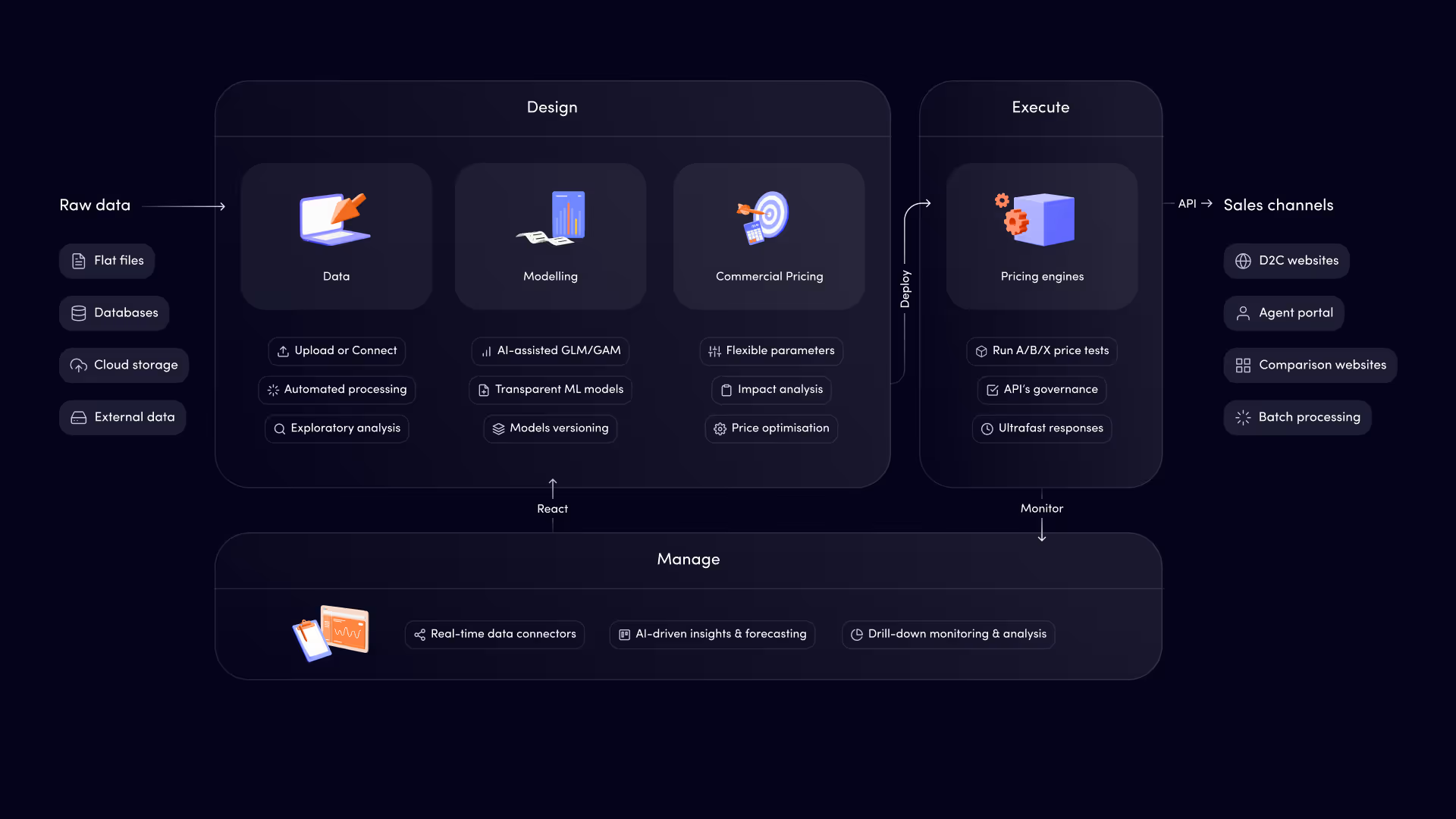

Integrated reaction & forecasting

Having portfolio monitoring dashboards and/or automated portfolio alerts has tremendous benefits for insurers. There is yet another step in portfolio management sophistication that can be used to improve LR/CoR for selected business lines.

Having portfolio management tools directly integrated with analytical environments in which risk, demand and pricing models are created facilitates quick reactions to any dynamics of the insurance portfolio.

This integration allows pricing executives to work together with analysts in a collaborative manner. It makes them recognize the events in the portfolio, adjust the pricing strategies and forecast the impact at a pace that allows them to have a competitive edge in the market. We can consider it as an ultimate goal for the chief of pricing in every insurance carrier when it comes to effective pricing strategy.

A simple recipe

A simple recipe for successful insurance portfolio management:

- Data first – catch up with both quotation/conversion data sources updated in real-time as well as others such as claims/financial/external.

- Invest in dedicated solutions to perform portfolio monitoring tailored to your business line needs.

- Go further with pricing sophistication, considering portfolio alerts and integrated ecosystem with modelling environment to early spot outliers in the portfolio and react with updated pricing strategy.

Need help? The Quantee team is happy to help you with our expertise and software to build a robust portfolio management experience.

%2520(2).avif)